Amazon and Shopify Now Half of US eCommerce

In the US, nearly 50% of ecommerce flows through Amazon and Shopify platforms. Amazon remains significantly larger in absolute scale, but Shopify continues to grow strongly year on year.

Market structure varies by geography. In the UK, ecommerce is more fragmented. Grocery retailers such as Tesco, Sainsbury’s and Asda own significant online share, while apparel specialists such as ASOS also own share in their respective categories.

The emergence of agentic commerce introduces further uncertainty. If large language models increasingly become the interface through which consumers shop, power may shift from storefronts to infrastructure. In that scenario, ownership of payments, inventory systems and merchant backends becomes more important than website traffic.

Shopify could be uniquely positioned in such a shift. It controls the merchant operating layer across millions of stores. If LLMs integrate directly into that infrastructure, Shopify becomes a commerce network rather than simply a website platform.

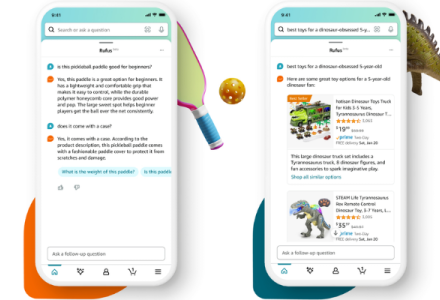

Amazon, however, operates at a completely different scale. As a closed ecosystem with vast catalogue depth, fulfilment capability and embedded consumer trust, it can internalise the agent layer. Early integrations such as Rufus demonstrate how Amazon may embed AI directly into the retail journey. If Amazon builds and controls its own shopping agents, this could reinforce rather than weaken its dominance.

Shopify increases competitiveness within the ecosystem, which is healthy from a market perspective. However, Amazon’s structural advantages in logistics, data and consumer habit suggest it is still well positioned to extend its leadership unless the agent layer meaningfully decentralises commerce.